If you or a loved one needs a hospital bed at home, you have probably come across the code E0303. It sounds technical. It sounds boring. But understanding it can save you thousands of dollars.

This guide walks you through everything you need to know about E0303 coverage requirements. We will keep things simple, clear, and useful. No confusing medical jargon. No hidden tricks. Just honest information to help you make the right decision.

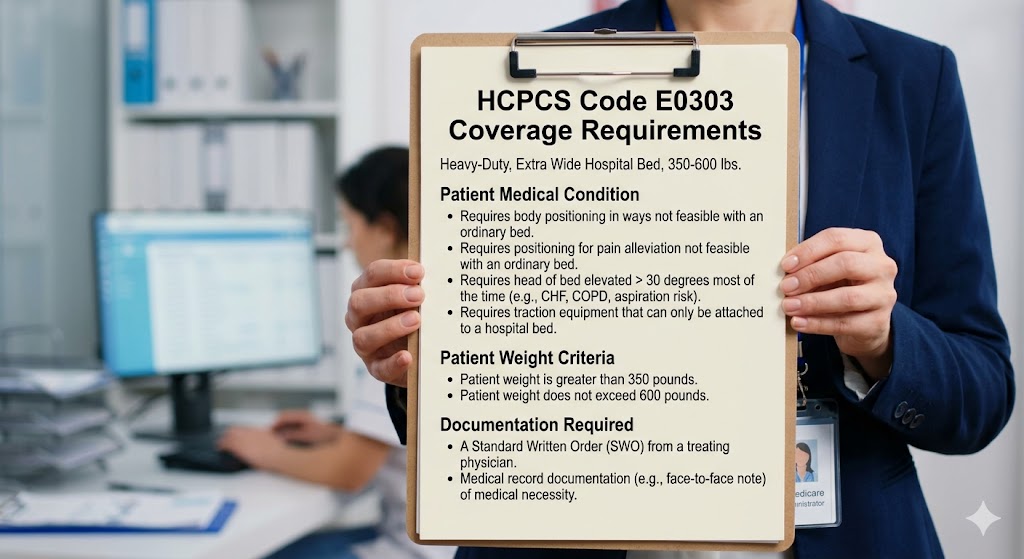

What Exactly Is E0303?

E0303 is a billing code used by Medicare and other insurance companies. It stands for a heavy-duty, extra-wide hospital bed. These beds are designed for patients who weigh more than 350 pounds. They are also wider than standard hospital beds.

Think of it this way:

- A standard hospital bed is 36 inches wide.

- An E0303 bed is at least 40 inches wide.

- It has a stronger frame and a more powerful motor.

These beds are not luxury items. They are medical necessities for people who need safe, comfortable support at home.

Important note: E0303 is different from E0296 (standard hospital bed) and E0304 (heavy-duty bed without extra width). Knowing the difference matters for your insurance claim.

E0303 Coverage Requirements: The Core Criteria

Now, let us talk about what actually gets your bed approved. Insurance companies do not hand out hospital beds like candy. You need to prove medical necessity.

Here are the main requirements for E0303 coverage:

1. Medical Necessity Documentation

Your doctor must write a detailed prescription. This is not a simple note that says “patient needs a bed.” It must explain:

- Why a standard bed is not safe

- Why you need extra width (usually due to body size or positioning needs)

- What specific medical condition requires the bed

2. Weight and Size Qualifications

Most insurers follow Medicare’s lead. For E0303 coverage, the patient typically needs to:

- Weigh more than 350 pounds

- Have a body width that requires more than 36 inches of sleeping surface

- Show that a standard bed would create safety risks (falls, pressure sores, entrapment)

3. Home Environment Assessment

An occupational therapist or durable medical equipment (DME) supplier may need to visit your home. They check:

- Doorway widths (the bed must fit)

- Floor space (room for the bed and turning radius)

- Electrical outlets (for the motor)

- Safety factors (rugs, pets, stairs)

4. Other Medical Conditions

Even if you meet the weight requirement, you still need an underlying medical condition. Common qualifying conditions include:

- Severe arthritis limiting mobility

- Chronic obstructive pulmonary disease (COPD) requiring head elevation

- Congestive heart failure with fluid management needs

- Neurological disorders (Parkinson’s, MS, ALS)

- Pressure ulcers or risk of developing them

5. Failure of Standard Equipment

Insurers want to know you tried simpler options first. Documentation should show that:

- A standard hospital bed (E0296) was tried but did not work

- Regular mattress overlays or supports failed

- Caregiver injuries occurred due to lifting or transferring

“We see too many denials because doctors write vague prescriptions. Be specific. Say exactly why a 36-inch bed is unsafe and how a 40-inch bed solves that problem.” — DME billing specialist, 22 years experience.

Table of Contents

- Pediatric Hospital Bed Rental Costs (detailed pricing and options)

- Semi-Electric Bed Insurance Coverage (what is covered and what is not)

- Step-by-Step Approval Process

- Common Denial Reasons and How to Appeal

- Medicare vs. Private Insurance for E0303

- Tips for Working with Your DME Supplier

- Frequently Asked Questions

- Additional Resources

Pediatric Hospital Bed Rental Costs

You might be wondering: why talk about pediatric beds in an article about E0303? Good question.

Pediatric hospital beds use different codes. E0303 is for adults. But families often search for pediatric options when caring for a child at home. Understanding rental costs helps you compare options and budget correctly.

What Does a Pediatric Hospital Bed Cost to Rent?

Pediatric beds are smaller. They often have fun colors, adjustable side rails, and lower heights for safety. Rental prices vary widely based on:

- Your location (urban vs. rural)

- The supplier (national chain vs. local family business)

- Rental duration (weekly, monthly, long-term)

- Insurance coverage

Here is a realistic breakdown of pediatric hospital bed rental costs in the United States:

| Bed Type | Average Monthly Rental | Average Weekly Rental | Insurance Typically Covers? |

|---|---|---|---|

| Standard pediatric bed (manual) | $150 – $250 | $50 – $75 | Often yes, with prior auth |

| Semi-electric pediatric bed | $250 – $400 | $80 – $120 | Sometimes, with medical necessity |

| Full-electric pediatric bed | $400 – $600 | $120 – $180 | Rarely, only for severe cases |

| Low-height pediatric bed (for fall risk) | $200 – $350 | $70 – $100 | Often yes, with documentation |

Out-of-Pocket Costs Without Insurance

If you do not have insurance or your claim is denied, you can still rent. Many suppliers offer self-pay discounts. Expect to pay:

- $200 to $500 per month for a basic pediatric bed

- $500 to $900 per month for a fully electric, high-end model

Some non-profits and medical equipment loan closets offer free or low-cost rentals. Always ask.

Is Renting or Buying Better for Pediatric Beds?

This depends on how long your child needs the bed.

- Rent if: use is expected to be less than six months, or your child is growing quickly (you may need a different size soon).

- Buy if: use is expected to be more than one year, or you have good insurance that covers purchase outright.

Important note: Medicare does not cover pediatric hospital beds under standard Part B. Children typically need coverage through Medicaid, private insurance, or state children’s health programs (CHIP).

Hidden Costs to Watch For

When budgeting for a pediatric hospital bed rental, remember these extra expenses:

- Delivery and setup fees ($50 – $150)

- Training for caregivers (sometimes free, sometimes $25 – $75)

- Mattress rental (often separate, $50 – $150 per month)

- Side rails (may be billed as accessories)

- Damage waiver ($10 – $30 per month)

Always ask for a full quote in writing before signing anything.

Semi-Electric Bed Insurance Coverage

Now let us focus on semi-electric beds. These are popular because they balance cost and convenience.

A semi-electric bed has:

- An electric motor to raise and lower the head

- An electric motor to raise and lower the foot

- A manual crank to adjust the overall bed height

This is different from:

- Manual beds: all adjustments done by hand crank (cheapest, hardest for caregivers)

- Full-electric beds: all adjustments electric, including bed height (most expensive, easiest)

Does Insurance Cover Semi-Electric Beds?

Yes, but with conditions. For semi-electric bed insurance coverage to apply, you usually need to prove that a manual bed is not safe or practical.

Common justifications that work:

- The patient lives alone and cannot use a manual crank

- The caregiver has a back injury or physical limitation

- Frequent head-of-bed positioning is needed (for GERD, breathing issues, or tube feeding)

Medicare Coverage for Semi-Electric Beds

Medicare Part B covers durable medical equipment (DME) including hospital beds. But here is the catch:

- E0296 (standard hospital bed, manual) is covered with a doctor’s order.

- E0303 (heavy-duty, extra-wide) is covered if you meet the weight and medical necessity criteria.

- E0271 (semi-electric feature) is an add-on. Medicare may cover the semi-electric upgrade if a manual bed would cause harm.

In plain English: Medicare might pay for the bed frame but ask you to pay the difference for the electric motors.

| Feature | Medicare Covers? | Patient Responsibility |

|---|---|---|

| Basic manual bed frame | Yes, after deductible | 20% coinsurance |

| Semi-electric upgrade | Sometimes, with documentation | Often 20% of upgrade cost |

| Full-electric upgrade | Rarely | Usually 100% out-of-pocket |

Private Insurance Semi-Electric Bed Coverage

Private insurers (Blue Cross, Aetna, UnitedHealthcare, Cigna, etc.) each have their own rules. However, most follow Medicare’s lead. Some actually offer better coverage.

What to check in your policy:

- Does your plan have a DME benefit?

- Is prior authorization required? (almost always yes)

- Are there in-network suppliers only?

- What is your deductible and coinsurance?

Realistic advice: Call your insurance company before renting anything. Ask specifically: “Is code E0303 covered if my doctor prescribes it with semi-electric controls?” Get a reference number for the call.

How Much Will You Pay Out-of-Pocket?

Even with insurance, you will likely pay something. Here is a realistic example:

- Semi-electric hospital bed retail price: $1,200 – $2,500

- Insurance allowed amount (negotiated rate): $900 – $1,800

- Your 20% coinsurance: $180 – $360

- Your remaining deductible: $0 – $500 (depending on how much you have already paid this year)

Bottom line: expect to pay between $200 and $800 out-of-pocket for a semi-electric bed with good insurance.

Without insurance? You pay full retail: $1,200 to $3,500.

Tips to Maximize Semi-Electric Bed Insurance Coverage

- Get a detailed letter of medical necessity. Mention specific tasks the caregiver cannot do manually.

- Try a manual bed first (even for a few days) and document the difficulties.

- Use an in-network DME supplier. Out-of-network claims are often denied or paid at lower rates.

- Ask about rent-to-own options. Many suppliers apply 80-100% of rental fees toward purchase.

- Appeal if denied. First denials are common. A simple appeal wins 40-60% of the time.

Step-by-Step E0303 Approval Process

Let us walk through the actual steps to get your E0303 bed approved. Follow these in order to avoid delays.

Step 1: Talk to Your Primary Doctor

Explain your needs. Bring up the specific code E0303. Ask if they have prescribed it before. If not, offer to provide information from this guide.

Step 2: Get a Face-to-Face Evaluation

Medicare requires a face-to-face visit within six months before ordering DME. Your doctor must document:

- Your diagnosis

- Your weight and body measurements

- Why a standard bed is insufficient

Step 3: Obtain a Written Order (Prescription)

The prescription must include:

- Patient name and date of birth

- Diagnosis code (ICD-10)

- Specific DME code (E0303)

- Duration of need (usually “long-term” or “lifetime”)

- Doctor’s signature and date

Step 4: Contact a Medicare-Approved DME Supplier

Not all suppliers are created equal. Search the Medicare supplier directory. Ask these questions:

- “Do you accept assignment for E0303?” (Yes = no surprise billing)

- “How many E0303 claims have you filed in the past year?”

- “Do you handle the prior authorization for me?”

Step 5: Submit the Claim (or Let Supplier Do It)

Most suppliers handle insurance billing for you. But you should still confirm:

- All forms are complete

- Medical records are attached

- The correct code is used

Step 6: Wait for Prior Authorization

Medicare takes about 30 days to review complex DME requests. Private insurance can take 7 to 21 days. Use this time to prepare your home for delivery.

Step 7: Delivery and Setup

Once approved, the supplier delivers the bed. They should:

- Assemble it

- Show you how to use controls

- Explain cleaning and maintenance

- Leave you a user manual

Step 8: Keep Documentation for Audits

Save every paper. Medicare audits DME claims up to seven years later. Keep:

- Doctor’s order

- Delivery receipt

- Proof of medical necessity

- Any appeal letters

Common Denial Reasons and How to Appeal

Denials happen. Do not panic. Most denials are fixable.

Top 5 Reasons for E0303 Denial

| Denial Reason | What It Means | Fix |

|---|---|---|

| Missing face-to-face visit | No documentation of exam within 6 months | Schedule visit, get retroactive note |

| Vague medical necessity letter | Just says “patient needs bed” | Rewrite with specific functional limits |

| Weight not documented | No recorded weight in medical record | Get current weight on clinic letterhead |

| Standard bed not tried | No failed trial documented | Document fall risk or caregiver injury |

| Supplier not enrolled in Medicare | Supplier is out-of-network | Switch to enrolled supplier |

How to Write an Appeal Letter

Keep your appeal letter simple. Use this template:

Date: [insert]

To: [Insurance company appeals department]

RE: Appeal for denied claim – [Patient name], ID [number]Dear Appeals Team,

*I am writing to appeal the denial of E0303 heavy-duty hospital bed. My doctor has confirmed medical necessity because [insert specific reason: weight over 350, width requirement, fall history].*

Attached you will find:

1. Updated doctor’s letter of medical necessity

2. Current weight documentation

3. Home safety assessment

4. Failed trial of standard bedPlease reconsider this claim. Thank you for your time.

Sincerely,

[Your name]

Send the appeal by certified mail. Keep a copy.

Appeal Timelines

- Medicare: 120 days to file appeal after denial

- Private insurance: typically 180 days

- Expected response: 30 to 60 days

Encouragement: Nearly 40% of first-level appeals for DME are approved. Do not give up.

Medicare vs. Private Insurance for E0303

Let us compare apples to apples.

Medicare (Original Part B)

| Aspect | Details |

|---|---|

| Coverage criteria | Strict, weight-focused, requires face-to-face |

| Supplier network | Any Medicare-enrolled supplier |

| Rental or purchase | Rent-to-own over 13 months |

| Patient cost | 20% after deductible ($240 deductible in 2025) |

| Appeal difficulty | Moderate, structured process |

Medicare Advantage (Part C)

| Aspect | Details |

|---|---|

| Coverage criteria | Varies by plan, may be stricter |

| Supplier network | Usually in-network only |

| Rental or purchase | Often purchase outright |

| Patient cost | Copay or coinsurance (varies widely) |

| Appeal difficulty | Higher, plan-specific rules |

Private Insurance

| Aspect | Details |

|---|---|

| Coverage criteria | Follows Medicare or looser |

| Supplier network | In-network strongly preferred |

| Rental or purchase | Either, depends on plan |

| Patient cost | Deductible + coinsurance (often 20-30%) |

| Appeal difficulty | Varies from easy (Cigna) to hard (some BCBS plans) |

Which is best for E0303 coverage?

Original Medicare is the most predictable for E0303. The rules are public and consistent. Private insurance may offer lower copays but more denials.

Tips for Working with Your DME Supplier

Your DME supplier can be your best friend or biggest headache. Choose wisely.

Green Flags (Good Suppliers)

- Answers the phone quickly

- Asks about your insurance before promising anything

- Offers to handle prior authorization for you

- Provides a written cost estimate

- Has been in business for 5+ years

- Has physical showroom where you can try beds

Red Flags (Avoid These)

- Demands full payment upfront before checking insurance

- Cannot tell you the exact billing code (E0303)

- Has multiple online complaints about billing fraud

- Pressures you to buy instead of rent

- No physical address listed

Questions to Ask Before Renting

- “What is my total monthly out-of-pocket cost after insurance?”

- “Is delivery and setup included?”

- “What happens if the bed breaks?”

- “Is there a rental cap (maximum months before I own it)?”

- “Can I exchange the bed for a different model if it does not work?”

Pro tip: Get every answer in writing. An email counts. A text message counts. Verbal promises over the phone are too easy to forget.

Frequently Asked Questions (FAQ)

Q1: What is the main difference between E0303 and E0304?

E0303 is heavy-duty AND extra-wide (40+ inches). E0304 is heavy-duty ONLY (standard 36-inch width). If you need width, use E0303.

Q2: Can I rent an E0303 bed without a doctor’s order?

No. Legitimate DME suppliers require a prescription. Anyone offering a hospital bed without an order is likely committing fraud.

Q3: How long does Medicare cover E0303 rental?

Medicare rents month-to-month for as long as medical necessity continues. After 13 months of continuous rental, you own the bed.

Q4: Does Medicaid cover E0303?

Yes, but each state has different rules. Contact your state Medicaid office. Some states require even stricter documentation than Medicare.

Q5: What if I weigh less than 350 pounds but still need a wide bed?

Some insurers make exceptions for body width alone. If your shoulders or hips exceed 36 inches, document that. Your doctor can argue “width-based necessity.”

Q6: Are mattress and accessories covered under E0303?

Typically no. The E0303 code covers only the bed frame. Mattresses, rails, trapeze bars, and overbed tables are separate codes with separate coverage rules.

Q7: Can I use my E0303 bed with a standard mattress?

No. You need a mattress designed for extra-wide beds (40+ inches). Standard twin or full mattresses will shift and create dangerous gaps.

Q8: What happens if Medicare denies my appeal?

You have two more appeal levels: reconsideration by a Qualified Independent Contractor (QIC) and an administrative law judge hearing. Few cases go that far, but some win.

Q9: Is there financial help if I cannot afford my share of costs?

Yes. Look for:

- Local Area Agency on Aging

- State DME loan programs

- Non-profits like The ALS Association or Arthritis Foundation

- Crowdfunding (GoFundMe has a medical category)

Q10: How often can I replace my E0303 bed?

Medicare expects a hospital bed to last 5 years. Replacement before that requires proof of wear, damage, or change in medical condition.

Additional Resource

For the most current Medicare DME coverage rules and supplier directory, visit the official Medicare.gov DME Coverage Database.

👉 Link: www.medicare.gov/coverage/hospital-beds-equipment-supplies (copy and paste into your browser)

This government resource lets you search by billing code (E0303), read local coverage determinations (LCDs) for your state, and find enrolled suppliers near you.

Important Notes for Readers (Do Not Skip)

📌 Note 1: Insurance rules change every year. The deductible amounts and coverage percentages mentioned here are accurate for 2025. Always verify with your specific plan.

📌 Note 2: Do not buy a used hospital bed from a private seller (Facebook Marketplace, Craigslist) without a prescription. You cannot get insurance reimbursement, and used beds may have hidden damage or recalls.

📌 Note 3: If a supplier offers to “waive your copay,” that is illegal. Suppliers cannot routinely waive Medicare coinsurance. It is considered fraud. Report them to 1-800-MEDICARE.

📌 Note 4: Keep a copy of your doctor’s order on your phone. If you travel or are admitted to a hospital, having proof of medical necessity prevents delays.

📌 Note 5: You have the right to choose any Medicare-enrolled DME supplier. Your doctor cannot force you to use a specific company.

Conclusion (Three Lines)

E0303 coverage requirements focus on medical necessity, patient weight above 350 pounds, and failed trials of standard beds. Semi-electric upgrades and pediatric rentals have separate rules but can be covered with strong documentation. Work closely with your doctor and an experienced DME supplier, appeal denials promptly, and do not pay upfront before insurance approval.